Howard Marks: The ‘Uncomfortably Idiosyncratic’ Billionaire [H/T

ValueWalk] (

LINK)

Related book: The Great Minds of Investing

Jana Vembunarayanan graciously shares his excelling "super videos" (

LINK)

The Brooklyn Investor comments on Brookfield Asset Management (

LINK)

Ben Bernanke joins the list of many who want to keep Alexander Hamilton on the $10 bill: Say it ain't so, Jack (

LINK)

Related book: Alexander Hamilton

A Dozen Things Learned from Peter Fenton About Business, Investing and Venture Capital (

LINK)

Chris Martenson talks to Jim Rogers (audio) (

LINK)

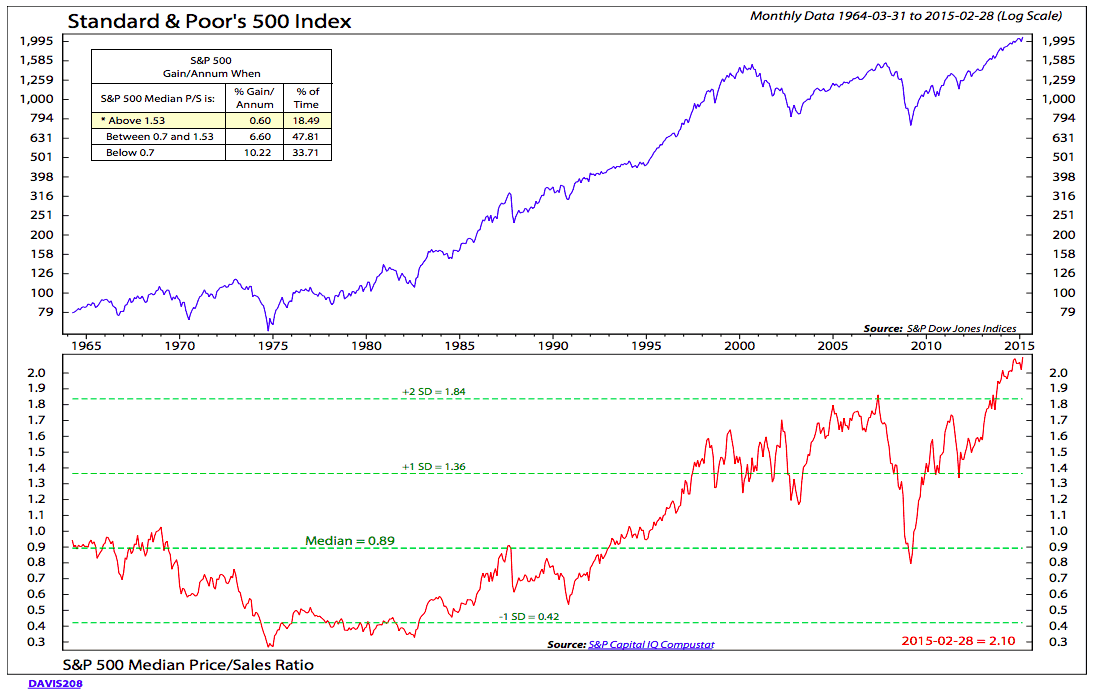

Hussman Weekly Market Comment: All Their Eggs in Janet's Basket (

LINK)

The financial markets are establishing an extreme that we expect investors will remember for the remainder of history, joining other memorable peers that include 1906, 1929, 1937, 1966, 1972, 2000 and 2007. The failure to recognize this moment as historic is largely because investors have been urged to believe things that aren’t true, have never been true, and can be demonstrated to be untrue across a century of history. The broad market has been in an extended distribution process for nearly a year (during which the NYSE Composite has gone nowhere) yet every marginal high or brief market burst seems infinitely important from a short-sighted perspective. Like other major peaks throughout history, we expect that these minor details will be forgotten within the sheer scope of what follows. And like other historical extremes, the beliefs that enable them are widely embraced as common knowledge, though there is always, always, some wrinkle that makes “this time” seem different. That is why history only rhymes. But in its broad refrain, this time is not different.

The central fallacy operating here is the notion that monetary easing provides a kind of mechanical and concrete support to the financial markets, when in fact the primary driver of financial markets in recent years has been pure speculative risk-seeking. While risk-seeking is encouraged by monetary easing, it is not a reliable outcome. Once speculative valuation extremes have been in place, persistent monetary easing has certainly not prevented severe market losses in prior cycles. Investor preferences toward risk distinguish the expanding phase of a bubble from its inevitable crash, and these are most directly measured through the behavior of market internals, not through the behavior of monetary authorities.

More enlightened leaders at the Federal Reserve would never have allowed, much less intentionally encouraged, yet the third speculative episode in 15 years. Unfortunately, the idea that repeated cycles of malinvestment and yield-seeking speculation have actually been the cause of the nation’s economic malaise doesn’t seem to cross their minds.

Book of the day:

The Greeks - by H. D. F. Kitto [Note: Unrelated to the reasons Greece is in the headlines today.]

Related to the book above is Charlie Munger's description of 'Curiosity Tendency' in

Poor Charlie's Almanack:

There is a lot of innate curiosity in mammals, but its nonhuman version is highest among apes and monkeys. Man's curiosity, in turn, is much stronger than that of his simian relatives. In advanced human civilization, culture greatly increases the effectiveness of curiosity in advancing knowledge. For instance, Athens (including its colony, Alexandria) developed much math and science out of pure curiosity while the Romans made almost no contribution to either math or science. They instead concentrated their attention on the "practical" engineering of mines, roads, aqueducts, etc. Curiosity, enhanced by the best of modern education (which is by definition a minority part in many places), much helps man to prevent or reduce bad consequences arising from other psychological tendencies. The curious are also provided with much fun and wisdom long after formal education has ended.

Re-reading that excerpt from Munger had reminded me of my post on

Areté, which led me back to

Zen and the Art of Motorcycle Maintenance and Kitto:

"What moves the Greek warrior to deeds of heroism," Kitto comments, "is not a sense of duty as we understand it... duty towards others: it is rather duty towards himself. He strives after that which we translate 'virtue' but is in Greek areté, 'excellence' — we shall have much to say about areté. It runs through Greek life."

...Kitto had more to say about this areté of the ancient Greeks. "When we meet areté in Plato," he said, "we translate it ‘virtue’ and consequently miss all the flavor of it. ‘Virtue,’ at least in modern English, is almost entirely a moral word;areté on the other hand, is used indifferently in all the categories, and simply means excellence."

{kind=link}